So, are we in a bubble?

– Banyan Tree Research

No doubt, Australian equity markets have seen substantial performance over a short timeframe. The Australian equity market has increased +29.5%, +10.7%, +12.1%, over 1-, 3-, and 5-year respectively (Figure 2). Likewise, World equity markets have increased +34.4%, +15.3%, +16.1%, over 1-, 3-, and 5-year respectively.

Figure 1: Global Markets Overview

Source: Banyantree, Bloomberg, Factset, Refinitiv; Pricing COB 24/09/21

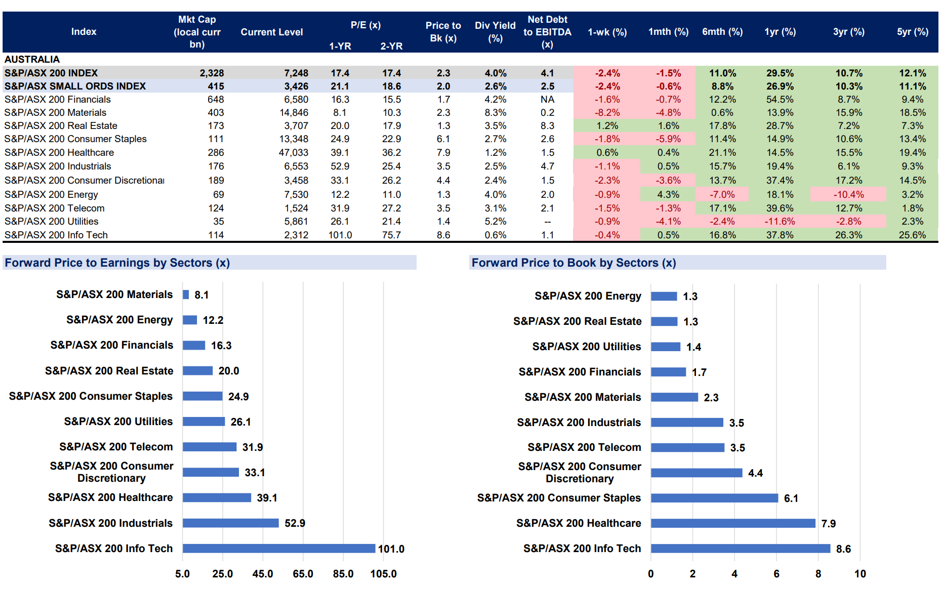

Figure 2: Australian Equity Markets

Source: Banyantree, Bloomberg, Factset, Refinitiv; Pricing COB 21/09/21

Australian equity markets now trade on 17.4x for 1- and 2-year forward price to earnings, 2.3x price to book, and 4.0% dividend yield (Figure 2). If we search the literature, we find protagonists on both sides of the debate armed with viewpoints, often seemingly rooted in financial theory, and drawing parallels to either classic bubble bursting moments or arguing for a continuation of the inflation of bubbles; to suit their narrative.

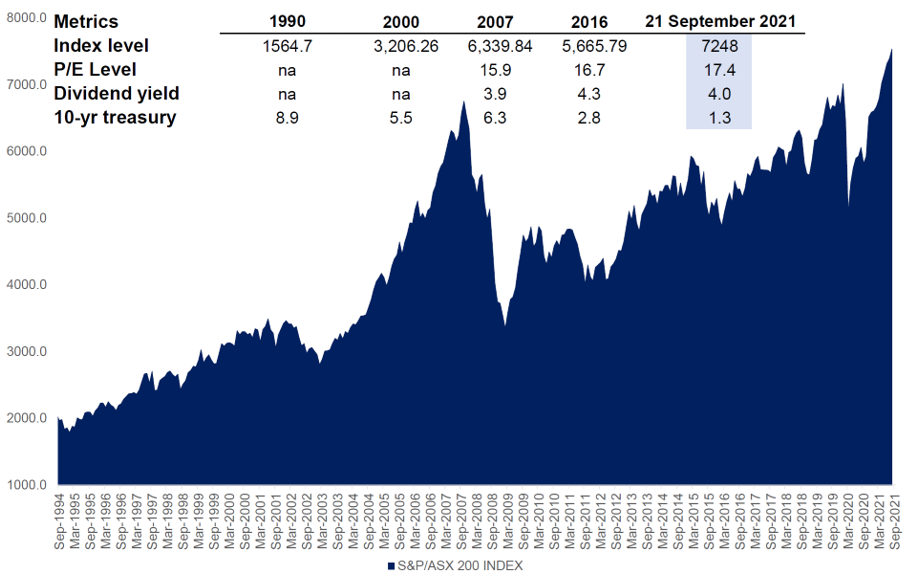

Indeed, zoom in and out of a chart of the historical prices of an index (Figure 3) and we can make a case for both sides. On the one hand, the fear-mongering/Bear narrative calls out an impending calamity due to:

– a combination of supposedly over stretched equity valuations;

– high corporate debt levels;

– a possible reversal in accommodative fiscal and monetary setting;

– heightened geopolitical tensions such as that stemming from trade wars (between China and U.S);

– trilateral security agreement (AUKUS) causing trade tensions;

– declining commodity prices (iron ore for instance), or

– contagion risks (in this instance, stemming from China Evergrande).

Figure 3: Australian Equity Markets – Trading Levels

Source: Banyantree, Bloomberg, Factset, Refinitiv; Pricing COB 21/09/21

Likewise on the other side, the Bull narrators highlight a combination of:

– ongoing economic policy settings remaining accommodative with no change in sight (this includes the substantial fiscal stimulus and low interest rate environment, in response to the Covid pandemic);

– valuations are not overstretched but rather frothy and justified considering the strength of corporates, and

– favourable macroeconomic indicators (sustainable and recovering GDP growth, low unemployment rates helped by government stimuli, manageable inflation rates, at least for the time being).

So, are we in a bubble? Our honest and short answer – we do not know (nor does anyone else know with certainty for that matter). Fortunately, in our view, the question of whether equity markets are in a bubble isn’t binary nor helpful in pondering, especially if it causes paralysis by analysis.

What we have been doing is managing risks so that the risks taken are commensurate with potential returns. We are focused on price discovery and taking advantage of the mismatch between intrinsic value and the share price on individual securities. In managing equity portfolios, we rely on our investment process, which focuses on stock selection and portfolio construction to manage any market scenario.

- Our approach has been unchanged in this current environment (see ‘Our investment process’ below)

- Taking profits by selling overpriced securities and redeploying it to mispriced stocks;

- Minimizing risk via diversification, and

- Focus on investing in mispriced quality companies.

The idea is that high quality companies have defensive earnings and other qualities which help them sustain their values at times of market distress.

Our investment process… we continue to filter, analyze, monitor and review stocks utilizing a bottom-up, fundamentals data driven process. We estimate a company’s worth in three assessments stages:

Filter #1: Quantitative Quality Assessment. The six quantitative factors we focus on: (1) Positive or improving revenue drivers over the long term; (2) Positive or improving EBITDA and margins over the long term; (3) Strong balance sheet for the sector over the long term; (4) Positive or improving free cash flow over the long term; (5) Positive or improving ROE over the long term; (6) Appropriate valuations – we do not categorise value or growth.

Filter #2: Qualitative Quality Assessment. The six qualitative factors we focus on: (1) the company being run by a solid management team; (2) minimal competition in the industry; (3) minimal potential of new entrants into the industry; (4) minimal power of suppliers; (5) minimal power of customers; (6) low threat of substitute products. Further, when appropriate, environmental, social and governance issues are also assessed.

Filter #3: Valuation Assessment. After determining ‘quality’ of a company, we assess value using a range of valuation methods rooted in financial theory. A financial model underpins each individual stock analysed.